How interest rate impact housing prices.

In this article we show how the changing interest rate impacts the housing market, as rising interest rate shift larger portion of the monthly payment towards interest and less toward principal, i.e. price of the house.

There is two way to buy things, cash or installments. And if you have to "finance" (the installment option) a purchase then the creditor (the person who is going to give you the loan) is concerned with two things, return on the money (interest rate of the loan) and the return of the money, i.e. the actual principal he or she let you borrow.

And these two risks are usually mitigated by two things, collateral and ability to pay back the loan. The former means usually some back up plan that allows the creditor to recover the money (say repo the house). The latter means some kind of income on your part.

Since most people do not have enough cash to buy their homes out right, the vast majority of them resort to borrowing. And how much money one can borrow is usually related to the ratio of the monthly payment they have to come with, and their income.

Let us consider the following example. Let us say you come to me and ask to borrow $1000 or so for a year. I ask you how you are going to pay me back, you say $100 a month and that is the maximum you can pay each month. Let us say I want to charge you 10% on that loan and let us see how the math works.

And if I want to get 10% return on my money, and you are capped at $100/month, the maximum amount you can borrow is $ 1090.90

However if for some reason I wanted to make 20% on my money, then that means the largest amount I can let you borrow (from me at least) is $1000 even. So you see how rising rates reduced the amount you can borrow.

Now think about it from the buyer perspective. As interest rate rise, they can borrow less. And if they can borrow less, they can afford less. So, the same person who might normally afford to bid on a $250k house based on his/her income, now can bid on $230k for example. That depends on what the interest rate was and what it changed to.

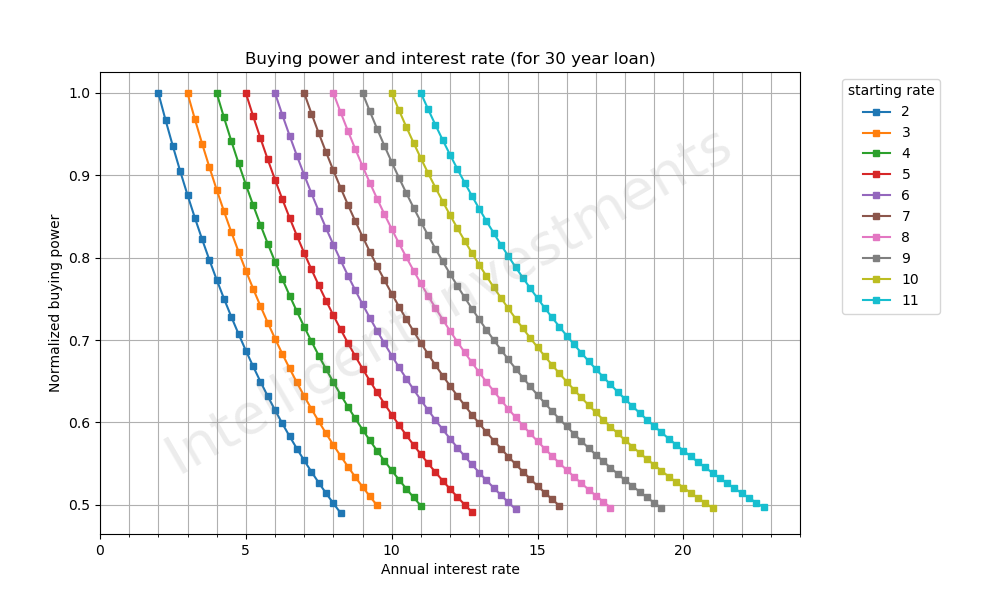

That is what the plot below helps answer. Each curve represents a starting and ending interest rate. These are shown on the x-axis. On the Y-axis is the normalized (or percentage) reduction of the buying power. So for example, let us take the curve marked 5. That means the starting interest rate was 5%. Now, if the interest rate rises 1.5% to 6.5% you can see on the y-axis how the buying power get reduced to 85%. So the same buyer who would qualify for $300k loan if the interest rate were 5% will now qualify for only $255k if the interest rate is 6.5%. And if the interest rate went from 5% to 8% then that buyer will qualify for about $220k, or 73% of what he/she used to.

And as buyers qualify for less and less, the homes bids have to go down. And all the sudden the person who bought his/her house based on the 5% loan, and has to sell it, is not going to get but the $220 the new buyers qualify for under the new rate.

Read More (not and active link)